Prediction Markets: Hyperliquid Outcome Contracts vs Polymarket and Kalshi

Prediction Markets: Hyperliquid Outcome Contracts vs Polymarket and Kalshi

Why did Hyperliquid enter prediction markets? Compare outcome contracts, Polymarket, and Kalshi across settlement, composability, and more.

June 11, 2026 — 9 min read

Prediction markets used to be easy to categorize.

Kalshi was the regulated one, Polymarket was the more crypto-native one, and everyone else was building in their shadow.

Despite their differences, both built markets around the same idea: trade the probability of future events.

This map changed in 2026.

In May 2026, Hyperliquid launched HIP-4 introducing outcome contracts native to HyperCore, co-authored by Kalshi's own head of crypto, and settled ~$6M on day 1.

This pops up a million questions:

> Are these outcome contracts a prediction market clone?

> Why is Hyperliquid, the #1 perpetual DEX, suddenly doing this?

> Are Polymarket and Kalshi competing with Hyperliquid?

Let’s answer all the questions one-by-one.

Before that, let’s learn how prediction markets work, differences in platforms’ approaches, and why those differences matter.

What Are Prediction Markets?

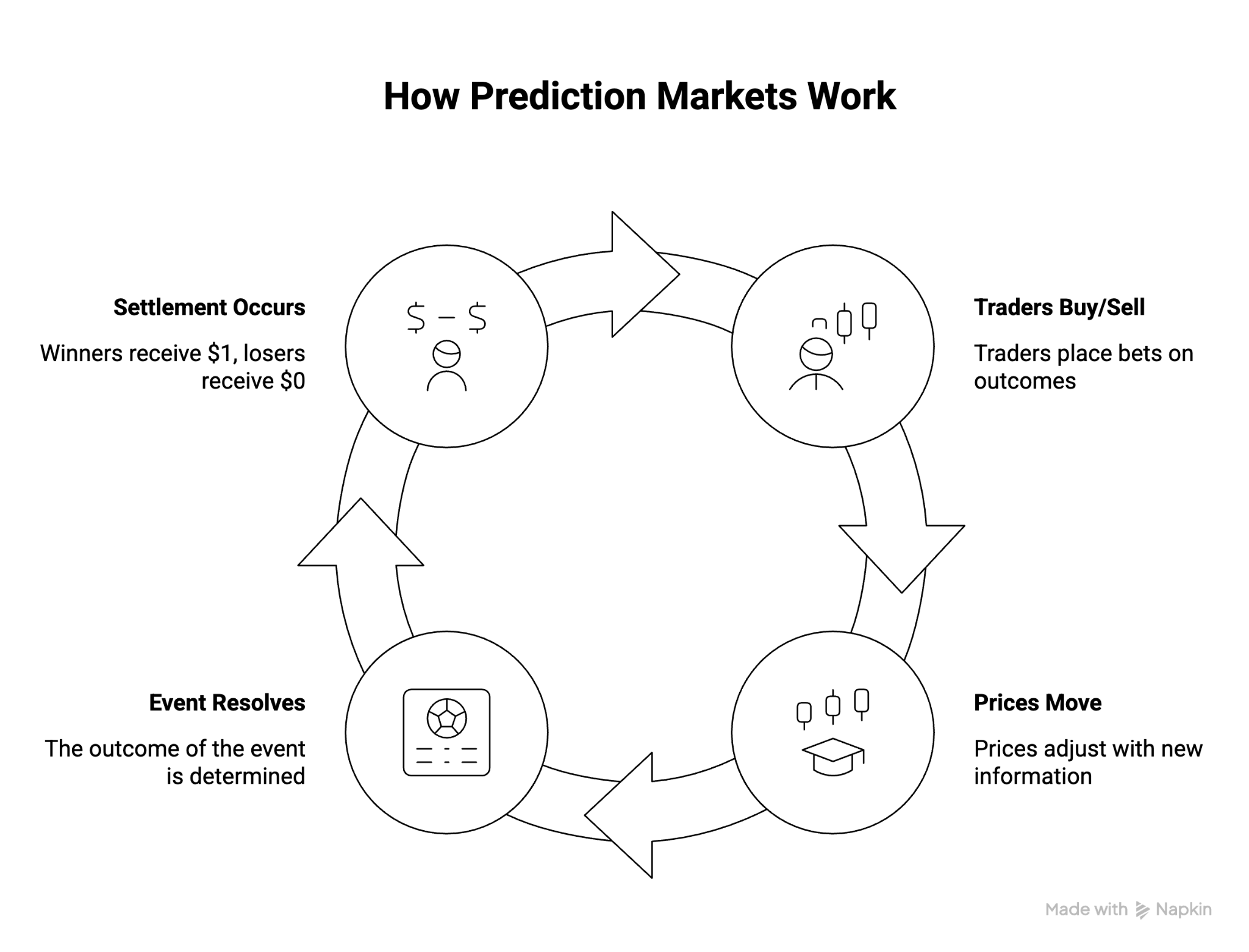

Prediction markets are exchanges where people trade contracts on the probability of a future event or outcome.

A standard market asks a binary question: Will the Federal Reserve cut interest rates in September?

Post that, it’s a simple price discovery as people buy and sell contracts based on their predictions until the event finishes and the market settles.

Here’s a simple snapshot:

These simple prediction and settlement mechanisms are the foundation for prediction markets generating $63.5 billion in volume in 2025.

Now, given Polymarket and Kalshi are dominating the market, why did Hyperliquid, the largest perpetual DEX, decide that prediction markets were worth building?

Let’s learn.

Current Approaches to Building Prediction Markets

Prediction markets are all the same: Traders speculate on future outcomes, prices update as information changes, and contracts eventually settle.

Surface-level, yes.

However, under the hood, the platforms are unique in terms of who can participate, how markets resolve, where liquidity forms, and what developers can build on top.

To make sense of what Hyperliquid is trying to do with HIP-4 and outcome contracts, it only is sensible to understand the status quo: Polymarket and Kalshi.

How Polymarket Works

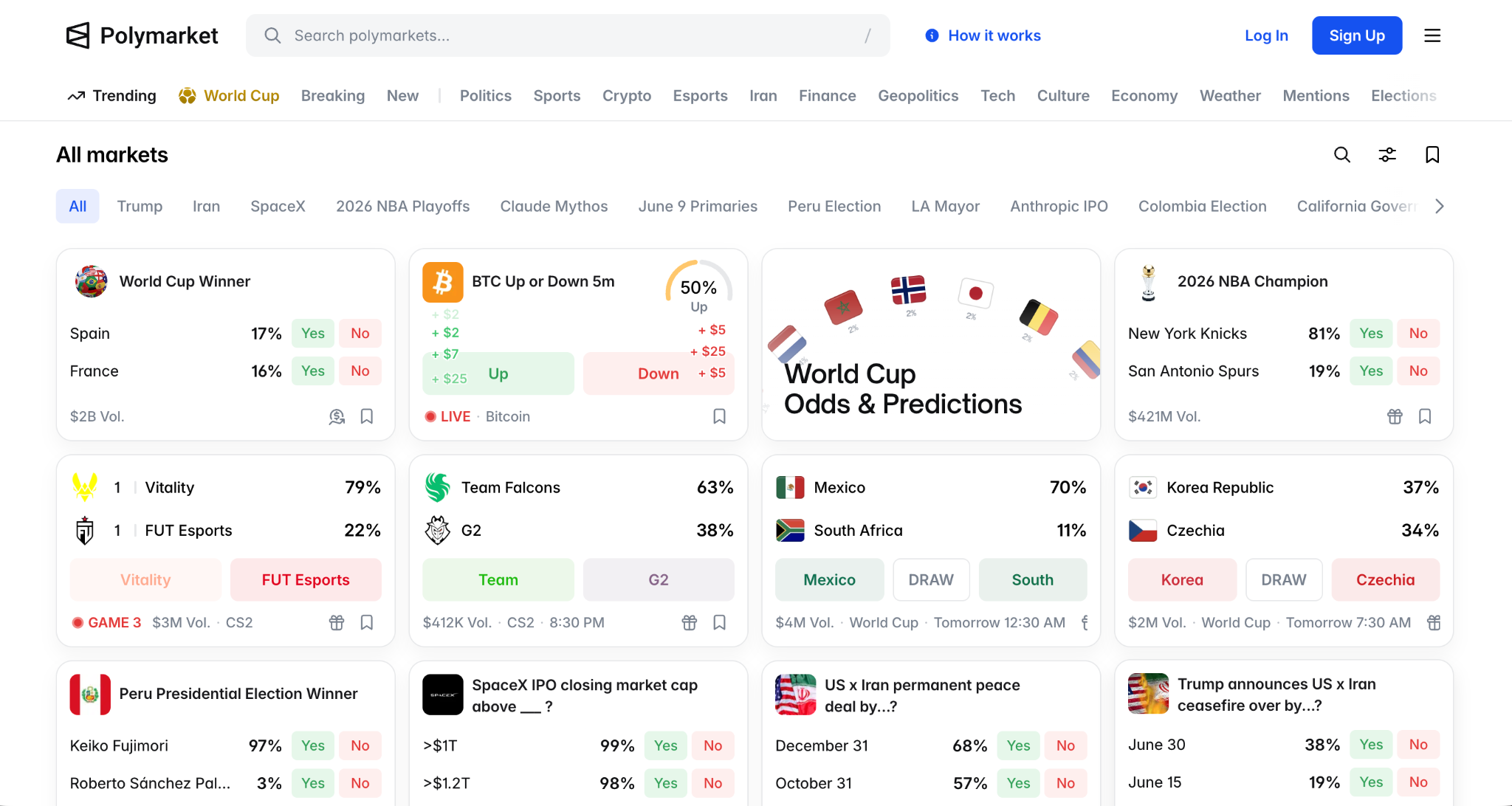

Polymarket built prediction markets as information markets.

Technically, Polymarket runs on Polygon with USDC collateral and resolves markets through UMA, an optimistic oracle where outcomes can be disputed before they finalize. Most global users can trade without KYC or a brokerage account which is a key reason behind its $9 billion market volume in April 2026.

Market-wise, Polymarket’s breadth is the product.

Politics became its breakout category, but the model expanded naturally into global sports, geopolitics, economy milestones, and macroeconomic events.

The trade-off is that information markets require mechanisms for determining truth.

Market resolution relies on UMA's optimistic oracle process, introducing dispute windows and occasional controversy when outcomes are ambiguous.

How Kalshi Works

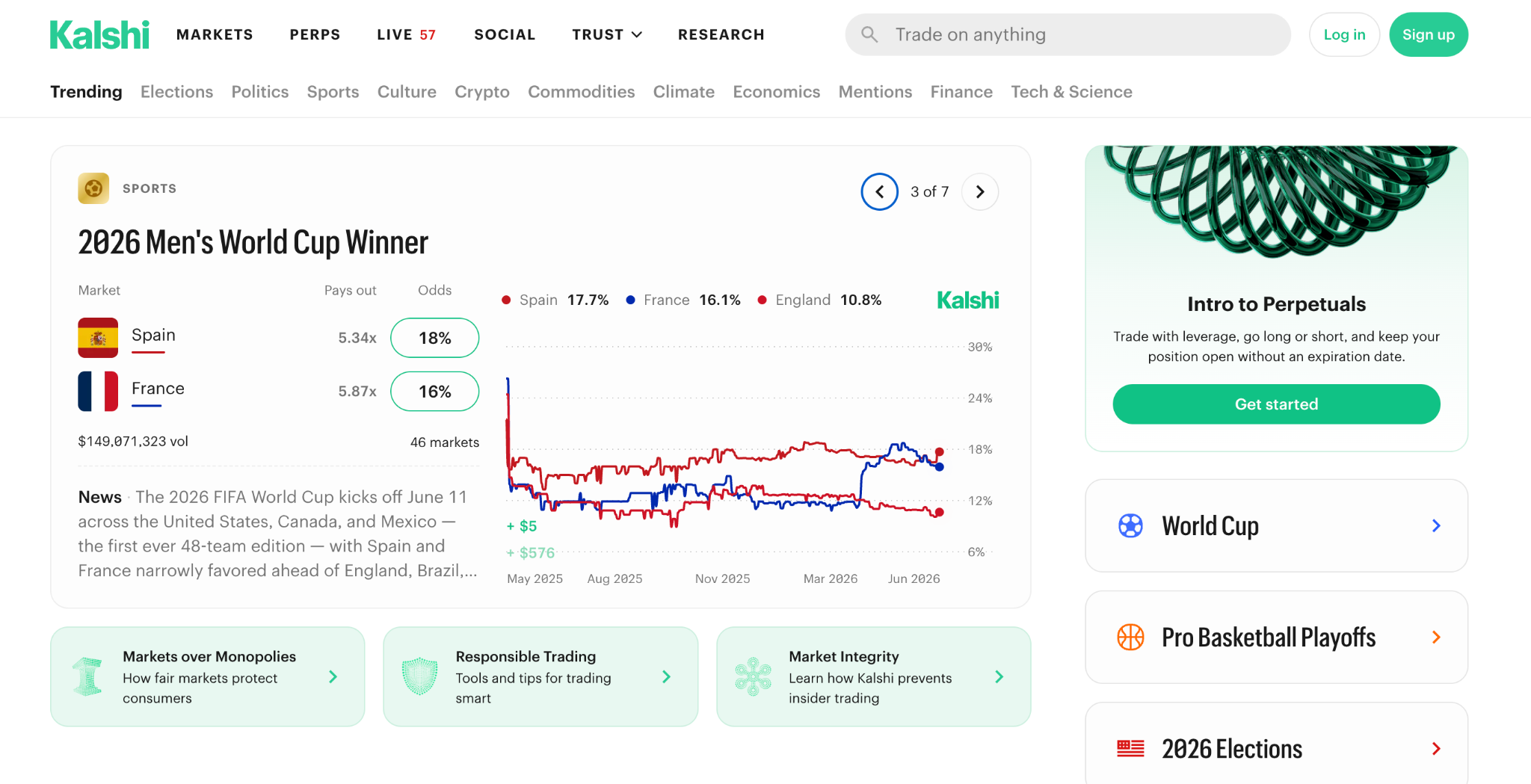

Kalshi built regulated event markets within the framework of US financial regulation.

As a CFTC-regulated exchange, Kalshi offers event contracts through familiar interfaces, fiat deposits, and compliance standards like traditional money platforms.

It resolves markets through a centralized board and distributes through Robinhood.

Kalshi is easier to access and participate in.

Users don't need wallets, stablecoins, or an understanding of oracle systems to participate. The platform expanded from politics and macroeconomic events into sports, where it now generates the majority of its trading activity.

Limitations of Kalshi is because of its regulatory priorities.

Market listings pass through regulatory guardrails, and users trade within a closed system rather than composable onchain infrastructure.

Similarly, transparency is lacking since a centralized board governs and decides on the market settlement and resolution.

Zooming out, Polymarket proved people would trade information. Kalshi proved they would do it within regulated rails.

Hyperliquid didn't have either problem to solve. It already had traders, liquidity, and one of the deepest derivatives venues in crypto.

So, how did Hyperliquid approach building outcome contracts?

Understanding Hyperliquid Outcome Contracts

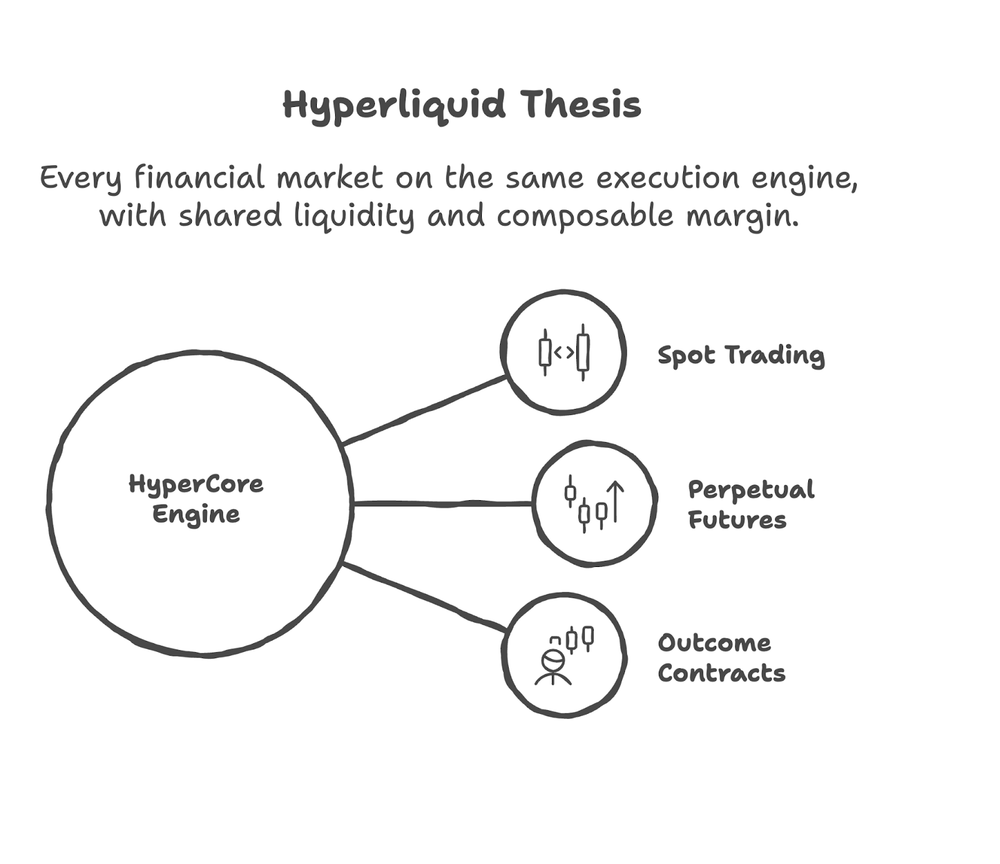

Hyperliquid didn't build a standalone prediction market.

HIP-4 introduced outcome contracts as a native instrument type inside HyperCore, the same execution environment that powers its perpetual futures markets.

Outcome contracts became another instrument for existing users who were trading perps, managing collateral, and expressing directional views.

For instance: A trader long BTC can also make a prediction on BTC’s year-end price from the same account using the same collateral pool.

Polymarket and Kalshi can't do this.

Each is a standalone venue. Prediction market positions live in isolation from the rest of a trader's portfolio.

Let’s understand each component of this in more detail.

What are Hyperliquid Outcome Contracts and How Do They Work

Outcome contracts are binary instruments tied to a specific event.

Each contract settles to either 0 or 1 depending on whether the stated outcome occurs.

If a contract asks, "Will the Federal Reserve keep rates unchanged in September?" and the answer is yes, holders of the YES side receive a payout of 1 while the NO side settles to 0.

HIP-4 uses a merged YES/NO order book: buying YES at price P is equivalent to selling NO at 1 minus P, so both sides draw from the same liquidity pool.

Learn more about HIP-4 and outcome contracts here

Why Hyperliquid Chose a Derivatives Model

Hyperliquid already had traders, liquidity, and an exchange processing billions of dollars in volume through a unified trading engine.

Building outcome contracts inside HyperCore meant users didn't have to bridge assets, open separate accounts, or learn a new interface to trade predictions.

The same collateral supporting perpetual futures positions could support outcome contracts. The same matching engine could price them.

Why Developers Should Care About HIP-4

HIP-4 and outcome contracts expand Hyperliquid's utility beyond just prediction markets.

Developers can monitor outcome creation via outcomeMeta, track validator votes via validatorL1Votes, and observe settlement via settledOutcome.

These help developers in building products that require prediction market positions to share margin with perpetual exposure: trading bots, macro hedges, event-driven automated strategies. Such interlaced products and interfaces are currently only possible on Hyperliquid.

Hyperliquid's thesis is that event contracts belong inside trading infrastructure. HIP-4 gives developers the primitives to test whether that's true.

Now that we know Hyperliquid’s product, build approach, and the future potential, let’s stack it up against the 2 popular platforms and compare.

Key Differences Between Hyperliquid, Polymarket, and Kalshi

Hyperliquid, Polymarket, and Kalshi let users trade future outcomes. The similarities largely end there.

Underneath, they differ in their assumptions about trust, settlement, collateral, access, and what prediction markets are ultimately meant to become.

The table below captures those distinctions.

Core Identity | Trading infrastructure | Information market | Regulated event exchange |

Blockchain |

Ofcourse, no single approach dominates across every dimension.

Each reflects a different answer to the same question: what should prediction markets optimize for?

The answer to that question will shape where the category goes next.

Now, where does the prediction market go from here?

The Future of Prediction Markets

Prediction markets are maturing as information infrastructure. And in the battle of the platforms, there may not be a single winner.

Users looking to discover what the market thinks about a niche geopolitical event may continue to gravitate toward Polymarket. Traders operating inside a regulated environment may prefer Kalshi. Active market participants already managing risk on an exchange may find Hyperliquid's approach more natural.

The more durable takeaway is that prediction markets are evolving beyond a category of their own.

The platforms that succeed will be the ones that integrate those functions into the systems people already trust and use.

FAQs: Frequently Asked Questions

Are Hyperliquid outcome contracts prediction markets?

Yes. Outcome contracts are binary instruments tied to future events and settle based on whether a specified outcome occurs. The difference lies in how they're integrated. Hyperliquid embeds them within an existing derivatives exchange rather than offering them through a standalone prediction platform.

How are Hyperliquid outcome contracts different from Polymarket?

Polymarket treats prediction markets as information markets. Hyperliquid treats event contracts as another trading instrument alongside perpetual futures.

The key structural differences are,

Composability (HIP-4 allows shared margin; Polymarket doesn't),

Order book design (HIP-4 uses a merged YES/NO book; Polymarket uses separate token books), and

Resolution model.

How are Hyperliquid outcome contracts different from Kalshi?

Kalshi operates as a CFTC-regulated event exchange with fiat rails and mainstream accessibility. Hyperliquid is crypto-native and optimized for composability and trading efficiency. One prioritizes regulatory certainty while the other prioritizes capital efficiency and integration with broader trading workflows.

Why did Hyperliquid launch HIP-4?

HIP-4 reflects Hyperliquid's belief that prediction markets don't need to exist as separate destinations. Event contracts can live alongside spot and derivatives products within the same trading environment.

How do Hyperliquid outcome contracts settle?

Markets settle to either 0 or 1 depending on whether the stated outcome occurs. Resolution criteria are defined when the market is created, and Hyperliquid validators participate in the settlement process through the protocol's native mechanisms.

Are prediction markets legal?

Legality depends on the jurisdiction and the platform. Kalshi operates under CFTC oversight in the United States. Crypto-native platforms such as Polymarket and Hyperliquid face different regulatory considerations depending on where users are located.

Which prediction market platform is most accurate?

Based on available data, Kalshi.

The 2025 Vanderbilt study found Kalshi at 78% accuracy versus 67% for Polymarket in the 2024 US presidential election. The gap reflects Kalshi's centralized resolution board and position size constraints, which reduce the impact of large individual traders on prices.

HIP-4 is too new to have comparable accuracy data.

Building on Hyperliquid with Quicknode

By offering managed Hyperliquid RPC endpoints, data access, and developer tooling, Quicknode allows teams to focus strictly on building products and solutions.

Quicknode's HyperCore integration, which is currently in public beta, promises to carry infra superpowers like:

Streams support for Hypercore datasets, enabling filtered, push-based delivery of Hyperliquid data

gRPC APIs designed for high-volume, low-latency data pipelines

JSON-RPC and WebSocket-related methods for compatibility with existing workflows

View current pricing: https://www.quicknode.com/api-credits/hyperliquid

More Quicknode resources for Hyperliquid builders:

Real-time risk monitoring and liquidation analytics API for HyperLend Protocol on Hyperliquid

Comparison of the top 6 Hyperliquid RPC providers for HyperCore and HyperEVM

SDKs & Tools

Hyperliquid Python SDK — also on PyPI

Hyperliquid API Examples — clone-and-run examples in Python, TypeScript, Rust & Go

Hyperliquid SDK Examples — advanced SDK usage patterns

HyperCore CLI — stream & backfill HyperCore data from the terminal

hyperliquidapi.com — zero-custody Hyperliquid trading API

For teams building on top of HIP-4, the infrastructure layer is the difference between a product that works when it matters and one that doesn't.

About Quicknode

Founded in 2017, Quicknode deploys institutional-grade blockchain infrastructure for developers and enterprises. With 99.99% uptime and support for 80+ chains, teams build and scale onchain applications without compromise.

Stay updated

The latest engineering insights, product updates, and web3 news delivered straight to your inbox.