Answers>Learn about blockchain basics>What is a blockchain?

What is a blockchain?

// Tags

blockchain definitionwhat is blockchainblockchain explained

TL;DR: A blockchain is a shared digital ledger that records transactions across a network of computers. No single person or company controls it. Once data is added, it can't be changed, making blockchains transparent, secure, and resistant to tampering.

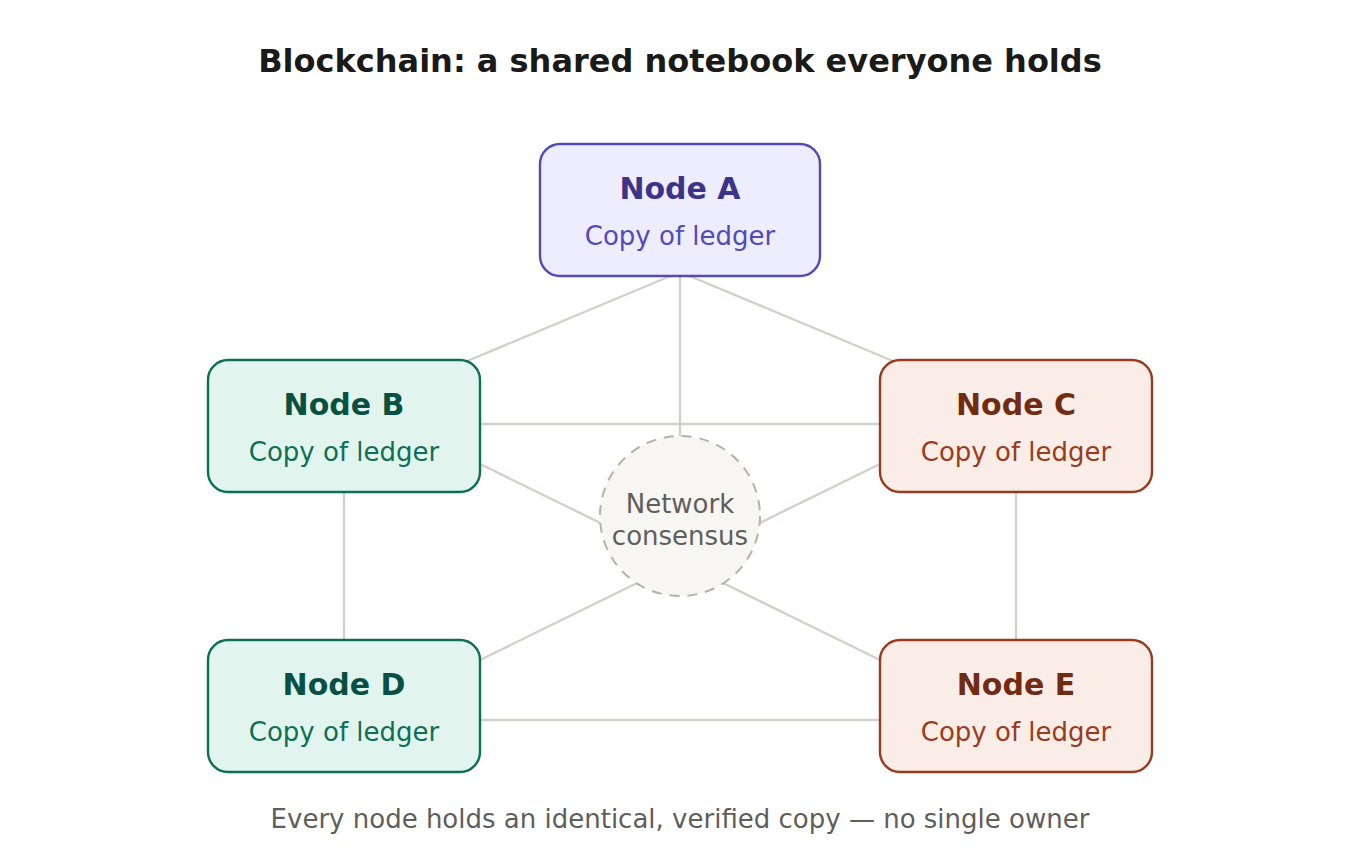

The Simple Explanation

Think of a blockchain as a shared notebook that thousands of people maintain at the same time. Every time someone makes a transaction (sending cryptocurrency, minting an NFT, or executing a smart contract) it gets written into this notebook. But instead of one person keeping the records, every participant in the network holds an identical copy.

This is what makes blockchain different from traditional databases. Banks, social media platforms, and governments all store your data on servers they control. That centralized setup creates a single point of failure: if the server goes down, gets hacked, or decides to restrict access, you're out of luck. Blockchain removes that vulnerability by distributing the data across potentially thousands of independent computers, called nodes.

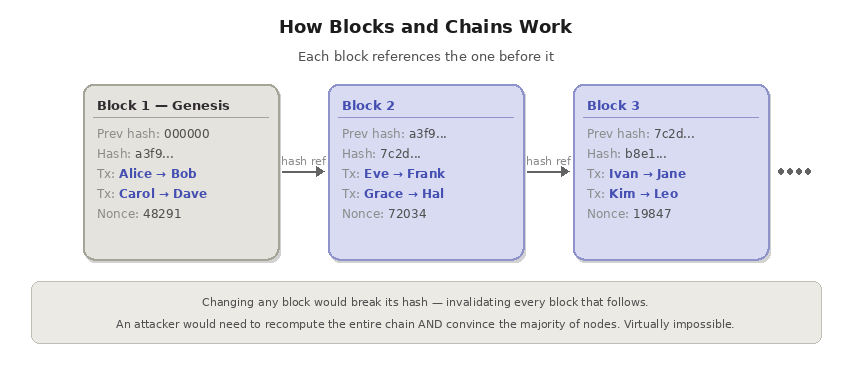

How Blocks and Chains Work

The name says it all. Transactions are grouped into blocks, and each block is linked to the one before it, forming a chain. When someone initiates a transaction, it's broadcast to the network. Nodes verify it using agreed upon rules called a consensus mechanism. Once verified, the transaction is bundled with others into a new block. That block receives a unique cryptographic fingerprint (a hash) that also references the previous block's hash. The block is then added to the chain, and every node updates its copy.

Because each block references the one before it, changing any historical data would require rewriting every subsequent block and convincing the majority of the network to accept it. On established networks, this is virtually impossible.

Why Blockchain Matters

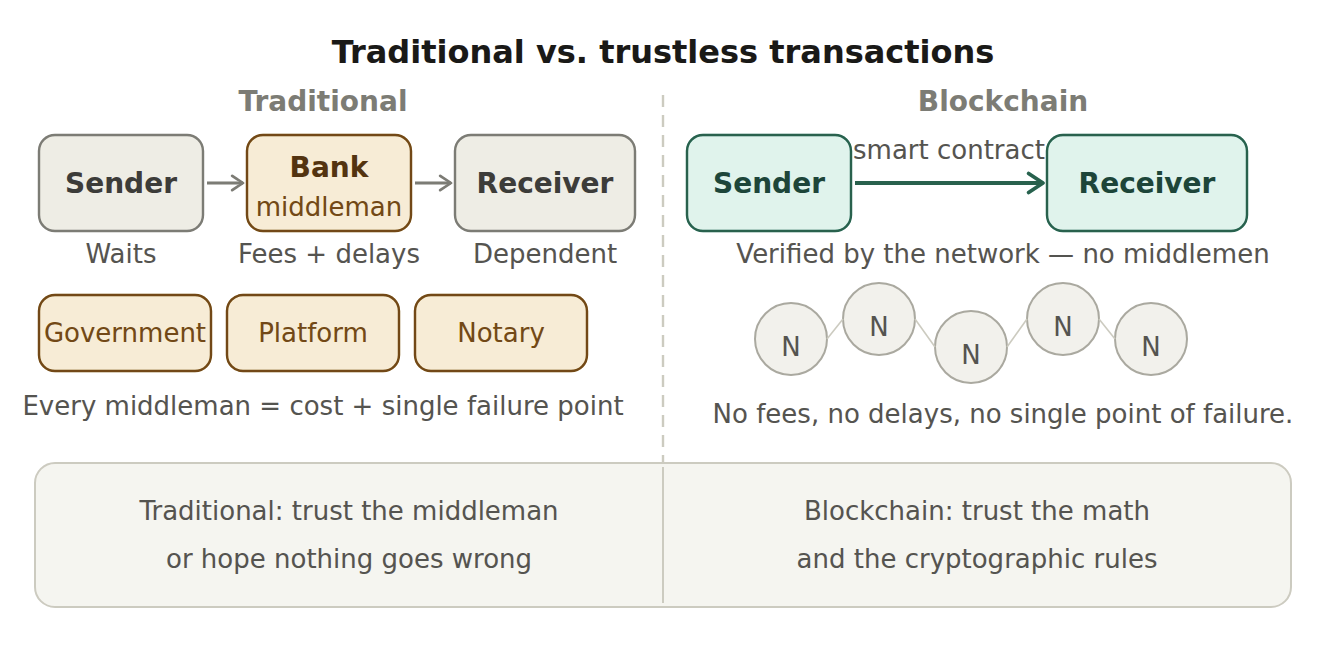

Blockchain solves a fundamental internet problem: how do you trust information when you don't trust the people sharing it?

Before blockchain, online trust required middlemen. Banks to verify payments, governments to certify documents, platforms to confirm identity. Each middleman added cost, time, and potential points of failure. Blockchain enables trustless transactions. You don't need to know or trust the other party, because the network's rules and cryptographic math guarantee integrity. This has opened the door to decentralized finance (DeFi), smart contracts, NFTs, and decentralized applications (dapps).

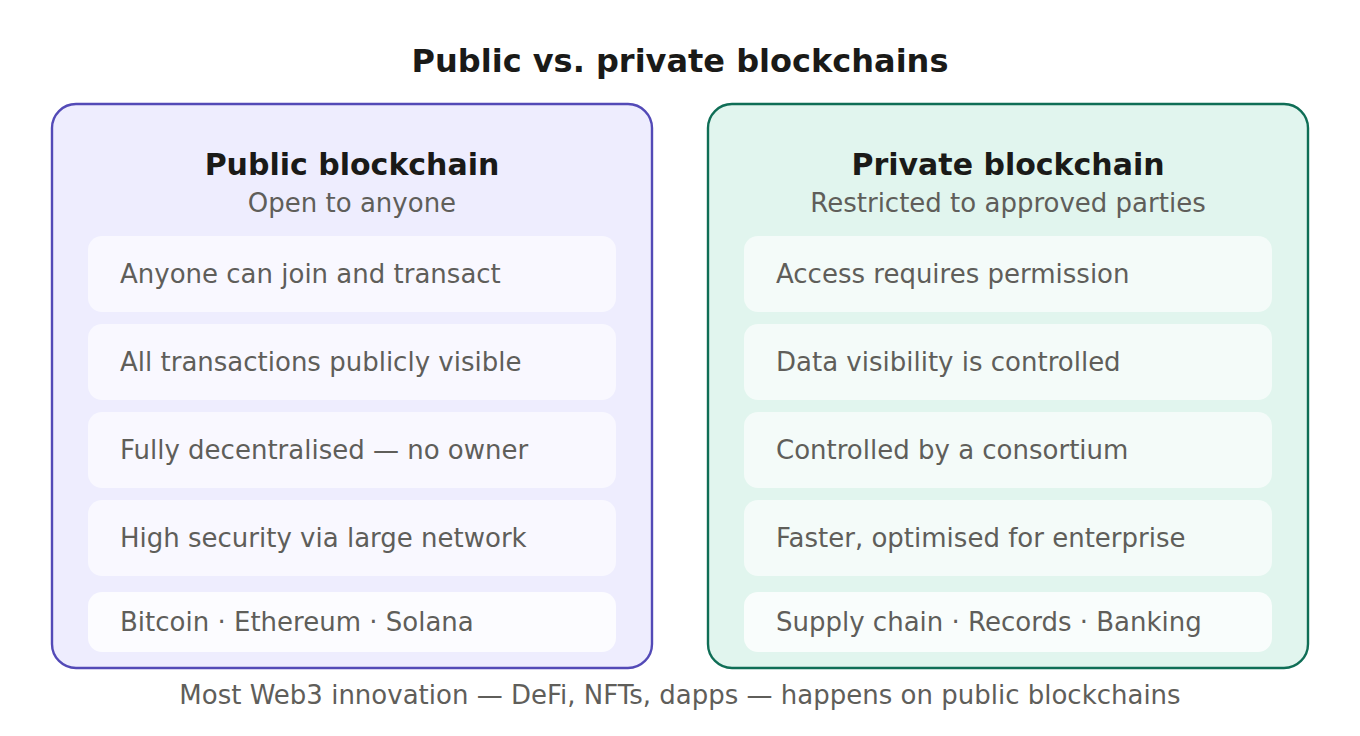

Public vs. Private Blockchains

Public blockchains (like Ethereum, Bitcoin, and Solana) are open to anyone. All transactions are visible and auditable. Private blockchains restrict participation to approved parties, often used by enterprises for supply chain tracking or internal record keeping.

Most Web3 innovation, and what developers build with Quicknode, happens on public blockchains.

Getting Started as a Developer

If you're building on blockchain, you interact with the network through RPC endpoints. These are connection points that let your code read from and write to the chain. Running your own node is complex, which is why infrastructure providers like Quicknode exist. Quicknode's Core API gives you instant access to 80+ chains so you can focus on your app, not your infrastructure.

What makes a blockchain secure?

A blockchain's security comes from three properties working together: cryptography, consensus, and decentralization. Each block carries a hash of the block before it, so altering an old record would change every hash that follows and instantly break the chain. To rewrite history an attacker would also need to control most of the network's mining power or staked value, which is the basis of a 51% attack.

Because copies of the ledger live on thousands of independent nodes, there is no single server to hack or shut down. Temporary disagreements between nodes can still happen and are resolved by the consensus rules. When the network briefly switches to a different version of recent history, the event is called a chain reorganization, and most blockchains settle these within a block or two.

How is a blockchain different from a traditional database?

Both store data, but they make very different trade-offs around control, trust, and how records can change. A traditional database is fast and flexible but relies on a central administrator. A blockchain is slower and append-only but removes the need to trust any single operator. The table below compares the two.

Property

Blockchain

Traditional database

Control

Distributed across many nodes

Owned by one organization

Trust model

Trustless, verified by math

Trust the administrator

Data changes

Append-only, effectively immutable

Create, update, and delete

Transparency

Public and auditable

Private and permissioned

Point of failure

No single point of failure

Central server

Speed

Lower throughput

Very high throughput

What are blockchains used for?

The first use case was digital money, but programmable chains expanded the design space far beyond payments. Self-executing smart contracts power decentralized finance, NFTs, on-chain games, and DAOs. Blockchains also underpin supply chain tracking, digital identity, and tokenized real-world assets.

As activity grew, base layers became congested, so much of this usage now happens on Layer 2 networks that batch transactions and settle them back to a main chain for lower fees and faster confirmations.

How do you interact with a blockchain?

You never talk to a blockchain directly. Your wallet or application sends requests to a blockchain node, which holds a copy of the ledger and broadcasts your transactions. Applications reach that node through an RPC endpoint, a simple URL that accepts standardized requests to read data or submit transactions.

Frequently Asked Questions

Is a blockchain the same as Bitcoin?

No. Bitcoin is one blockchain, and the first widely used one. Blockchain is the underlying technology, while Bitcoin is a specific network that uses it to record cryptocurrency transactions. Thousands of other blockchains, such as Ethereum and Solana, exist for different purposes.

Can data on a blockchain be deleted or changed?

In practice, no. Once a transaction is confirmed and buried under later blocks, rewriting it would require redoing the work of every block after it and overpowering the rest of the network. This is why blockchains are described as immutable, even though nothing is literally impossible to change.

Who controls a public blockchain?

No single entity does. The network is run by independent node operators and validators who follow shared consensus rules. Changes to those rules require broad agreement across the community, developers, and the operators who run the software.

Where are crypto assets actually stored?

Balances live on the blockchain itself, not inside your wallet. A crypto wallet stores the private keys that prove ownership and let you authorize transactions, so losing those keys means losing access to the assets.

Is blockchain only used for cryptocurrency?

No. While cryptocurrency was the first application, blockchains are now used for smart contracts, NFTs, supply chain provenance, identity, voting systems, and tokenized assets. Any record that benefits from being shared, tamper-evident, and verifiable can live on a blockchain.