Answers>Learn about MEV & transaction ordering>Why MEV exists

Why MEV exists

// Tags

why MEV exists MEV economics

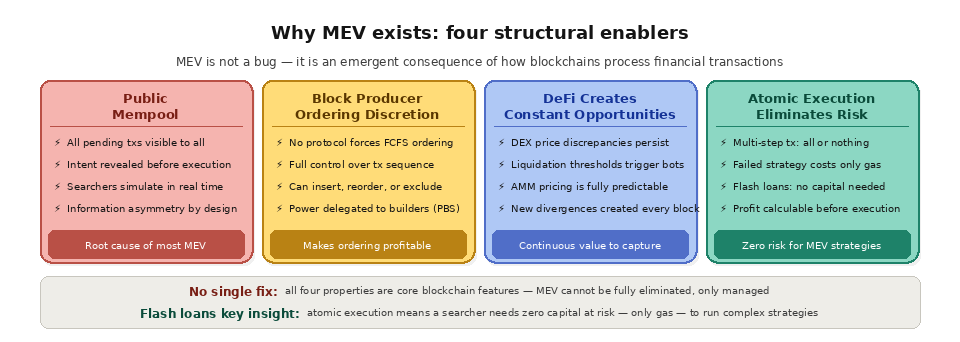

TL;DR: MEV exists because of four fundamental properties of blockchain architecture: public mempools that expose pending transactions before execution, block producer discretion over transaction ordering, DeFi protocols that continuously generate economic opportunities through price discrepancies and liquidation thresholds, and atomic execution guarantees that allow complex multi-step strategies to either fully succeed or fully revert with no risk of partial failure. These structural features combine to create an environment where informed actors can extract value from transaction ordering. MEV is not a bug in any single protocol. It is an emergent consequence of how blockchains process financial transactions in a transparent, programmable environment.

The Simple Explanation

To understand why MEV exists, you need to understand the unique combination of properties that blockchains offer to anyone willing to exploit them. No traditional financial system has all of these properties simultaneously, which is why MEV is a phenomenon specific to blockchain.

In traditional finance, order books are not public before execution. A stock exchange does not broadcast everyone's pending orders to the entire market before matching them. Market makers and high-frequency traders have information advantages, but the raw pending order flow is not universally visible. On a blockchain, every pending transaction sits in the public mempool, fully visible to anyone monitoring the network. A user's intent to swap $500,000 of ETH for USDC on Uniswap is broadcast to the world before it is executed. Any participant with the technical capability to monitor the mempool can see this transaction and react to it.

This transparency is a core design feature of blockchains, not a flaw. Decentralized networks need public transaction propagation so that validators across the world can receive, verify, and include transactions. But the same transparency that enables trustless verification also enables informed front-running by sophisticated actors.

Structural cause

Why it enables MEV

Public mempool

Pending transactions are visible before they execute

Ordering discretion

Block producers choose the sequence inside a block

DeFi activity

Price gaps and liquidations create constant opportunities

Atomic execution

Multi step strategies succeed fully or revert with no partial risk

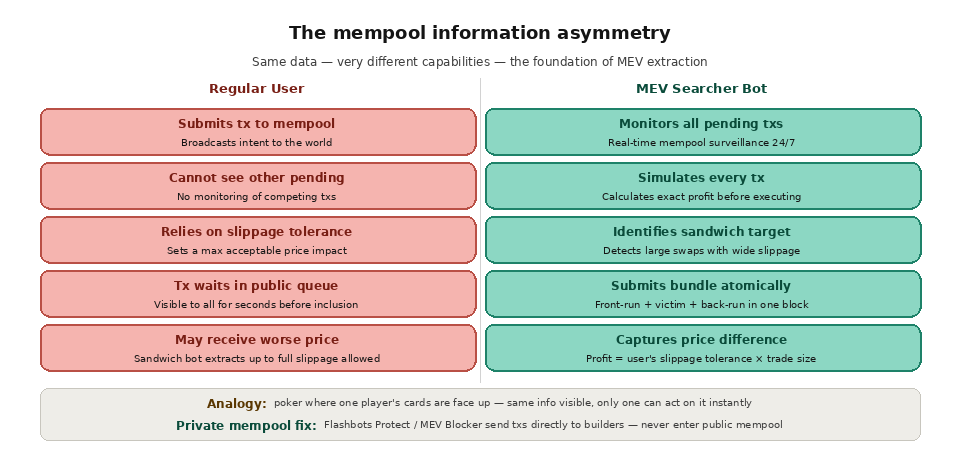

Public Mempools Create Information Asymmetry

The mempool is the root cause of most MEV. When a transaction enters the mempool, it reveals the sender's intent: what contract they are calling, what function they are executing, what parameters they are passing, and implicitly what price impact their action will have on onchain markets. This information is available to everyone, but only a small number of participants have the infrastructure and algorithms to act on it in real time.

A regular user submitting a swap on a DEX does not monitor the mempool. They do not know what other transactions are pending, how their transaction will interact with other pending trades, or whether a bot is about to sandwich them. A MEV searcher, by contrast, runs dedicated monitoring infrastructure that parses every pending transaction, simulates its execution against the current chain state, and calculates whether a profitable ordering opportunity exists. This information asymmetry, where both parties see the same data but only one can act on it effectively, is the foundation of MEV extraction.

The situation is analogous to a poker game where one player's cards are face up on the table. The cards are technically visible to everyone, but only the players who know how to read them and respond instantly gain an advantage.

Block Producers Control Ordering

The second structural enabler of MEV is that block producers have full discretion over how they order transactions within a block. There is no protocol-level rule that says transactions must be ordered by the time they were submitted, or by the sender's address, or by any other neutral criterion. The block producer can arrange transactions in any sequence they choose, as long as each transaction is valid given the state produced by the transactions before it.

This ordering power is absolute within a block. If a validator sees a pending transaction that will move a market, they can insert their own transaction before it, after it, or both. They can reorder unrelated transactions to create state conditions that make other transactions more or less profitable. They can exclude transactions entirely (though this has reputation and protocol implications).

In practice, most validators on Ethereum no longer exercise this ordering power directly. They delegate block building to specialized builders through Proposer-Builder Separation (PBS). But the underlying power remains: whoever constructs the block determines the order, and that order determines who profits and who loses.

DeFi Creates Continuous Economic Opportunities

MEV would not be worth extracting if there were nothing valuable to capture. The explosion of DeFi activity has created a constant stream of exploitable opportunities.

Price discrepancies between decentralized exchanges arise naturally because each pool prices assets based on its own reserve ratios. When a large trade moves the price on one DEX, the price on other DEXes does not update until someone arbitrages the difference. This creates a perpetual cycle: users trade, prices diverge, arbitrageurs correct them, new trades create new divergences. Every correction is an MEV opportunity.

Lending protocols like Aave and Compound create liquidation opportunities whenever a borrower's collateral ratio falls below the required threshold. The protocol incentivizes anyone to liquidate these positions by offering a discount on the seized collateral. During market downturns, hundreds of positions can become liquidatable simultaneously, creating a feeding frenzy among MEV bots competing to execute liquidations first.

Automated market makers with their predictable pricing curves make it mathematically straightforward to calculate the exact profit from any given trade sequence. Unlike traditional markets where order book depth and hidden liquidity create uncertainty, AMM pricing is fully deterministic and publicly visible. A searcher can calculate the exact profit from a sandwich attack before executing it, with zero uncertainty about the outcome.

Atomic Execution Eliminates Risk

The final structural enabler is blockchain's atomic execution model. When a smart contract transaction is submitted, it either executes completely or reverts entirely. There is no partial execution. This means a MEV strategy involving multiple steps (buy on DEX A, sell on DEX B, repay a flash loan) either succeeds in full and produces a profit, or fails and costs nothing beyond the gas fee for the reverted transaction.

This property is extraordinarily powerful for MEV extraction. In traditional finance, executing a multi-leg arbitrage involves execution risk at every step. You might buy the asset on one exchange but fail to sell it on another before the price moves. On a blockchain, the entire multi-step strategy executes within a single transaction. If any step fails, the entire transaction reverts, and you are back where you started (minus gas).

Flash loans amplify this property even further. A searcher can borrow millions of dollars, execute an arbitrage, repay the loan, and pocket the profit, all within a single atomic transaction. If the arbitrage does not produce enough profit to repay the loan, the entire transaction reverts including the borrow. This means MEV extraction requires no capital at risk beyond gas fees, dramatically lowering the barrier to entry for sophisticated strategies.

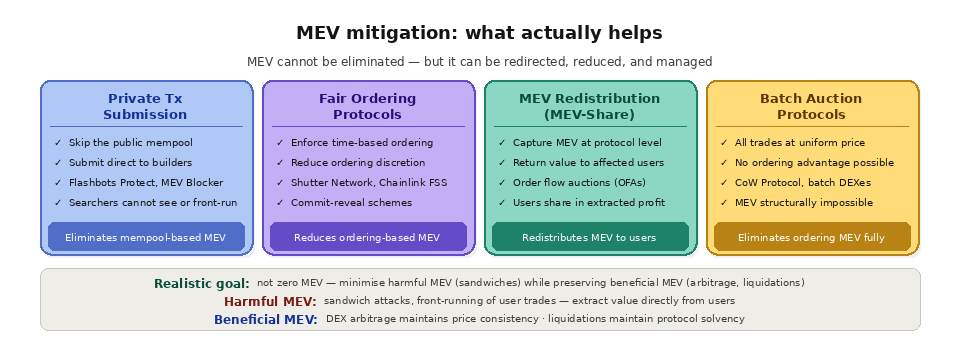

Can MEV Be Eliminated?

MEV cannot be fully eliminated as long as blockchains have public mempools, discretionary transaction ordering, and onchain financial activity. These are fundamental architectural properties, not configuration options that can be toggled off.

However, MEV can be mitigated, redistributed, and managed. Private transaction submission (through services like Flashbots Protect and MEV Blocker) prevents searchers from seeing transactions before execution, eliminating the mempool information advantage for those users. Fair ordering protocols attempt to enforce time-based ordering, reducing the value of ordering manipulation. MEV-Share and similar mechanisms redistribute captured MEV back to the users whose transactions generated it. Batch auction protocols like CoW Protocol execute all trades at a uniform clearing price, removing ordering-based extraction entirely.

The realistic goal is not zero MEV but minimizing the MEV that harms users (sandwich attacks, front-running) while preserving the MEV that benefits the ecosystem (arbitrage that maintains market efficiency, liquidations that maintain protocol solvency).

How Quicknode Helps Developers Understand MEV

Quicknode provides the infrastructure foundation for understanding and responding to MEV in production applications. The Core API's low-latency RPC access lets developers monitor mempool state, track gas price dynamics, and submit transactions with precise timing. Quicknode Streams delivers real-time block and transaction data with guaranteed delivery, enabling developers to build analytics systems that quantify MEV activity on their protocols, detect sandwich attacks against their users, and measure the ordering patterns within blocks that affect their applications.

For developers building DeFi protocols, the ability to analyze transaction ordering patterns through Streams data is essential for designing MEV-resistant mechanisms. For application developers, understanding MEV through real-time data informs better gas estimation, smarter transaction submission strategies, and more accurate user-facing price impact estimates. Quicknode's infrastructure ensures you have the data and the speed to make informed decisions in an MEV-aware blockchain environment.

Why does MEV not happen the same way in traditional finance?

Traditional markets hide pending orders, enforce ordering rules through regulated exchanges, and expose traders to execution risk on every leg of a trade. Blockchains invert all three: orders are public, ordering is at the block producer's discretion, and execution is atomic. That combination is what makes the broader phenomenon of MEV in blockchain possible in a way that simply does not exist in legacy finance.

Property

Traditional finance

Public blockchain

Pending orders

Hidden until matched

Visible in the public mempool

Ordering rules

Exchange enforced and regulated

Block producer discretion

Execution risk

Each leg can fail separately

Atomic, all or nothing

Who can react

A few privileged insiders

Anyone running a searcher bot

Who actually profits from MEV?

Three groups share the value. Searchers spot opportunities and build the transactions that capture them, builders assemble the most profitable block, and validators collect payment for proposing it. The common thread is control over transaction ordering, which is the lever every one of these participants ultimately depends on.

Can users and developers reduce their MEV exposure?

Yes. Users can route trades through private order flow, set tight slippage, and break up large swaps so bots have less to extract. A practical overview of MEV mitigation strategies lays out the options and their trade-offs.

Developers have an extra lever: the endpoint. Submitting transactions through a private or protected RPC endpoint keeps them out of the public mempool, which removes the visibility that most extraction depends on.

Is MEV the same on Layer 2 networks?

Not exactly. Most rollups today route transactions through a single sequencer rather than a public mempool, so classic front running is harder, but the sequencer itself holds the ordering power. As sequencers decentralize, the MEV picture on Layer 2 is expected to keep evolving.

Frequently Asked Questions

Is MEV a bug in the protocol?

No. MEV is an emergent result of public mempools, discretionary ordering, and onchain finance working together. No single protocol introduced it, and no single patch removes it.

Can MEV be eliminated completely?

Not while blockchains keep public mempools and discretionary ordering. It can be reduced and redistributed through private order flow, fair ordering, and batch auctions, but not erased.

Is all MEV bad for users?

No. Arbitrage and liquidations are healthy and keep markets and lending protocols functioning. Predatory forms like sandwich attacks are the harmful side that most mitigation efforts target.

Do flash loans cause MEV?

Flash loans do not create MEV, but they amplify it. Because a flash loan and the strategy it funds settle in one atomic transaction, searchers can chase large opportunities with almost no capital at risk.

Does MEV exist on Layer 2 networks?

Yes, in a different shape. A Layer 2 blockchain usually orders transactions through one sequencer, which changes who can extract value and how, compared to Ethereum mainnet.